ACM Commentary 2Q 2011

2ND QUARTER 2011 MARKET SUMMARY

Alamar is happy to report a second quarter return of 4.3% and a 12.8% return for the first half of the year. As we have mentioned in past writings, we are bottom up stock pickers at heart and much of our performance during the course of this year can be attributed to the performance of these stocks, as opposed to our collective weightings to any one sector, or industry group. As an example, we have been a bit under-weight the overall market in the consumer staples sector this year. However, a couple of our stocks in this area have done quite well in 2011, resulting in staples being the biggest contributor to our portfolios return thus far.

Our process involves breaking down the merits of one individual business at a time to determine whether or not to make an investment. It is our preference that sector weightings come as a byproduct of our stock picking analysis and not as a central theme. We expect this phenomenon to continue in the years to come, and believe it serves us well for two reasons. First, our reliance on companies, and specifically management teams, to help drive our performance makes us less dependent on, but not immune from, the performance of the economy. Secondly, our focus reduces the need to try to predict the future or “Time the Market”, which history has shown is very difficult to do! We do try to identify broad based, long lived demographic trends that make the future growth of earnings, sales, and cash flows of certain businesses more predictable over time. At Alamar we view our long term time horizon and our patience as two key competitive advantages.

We foresee spending much more time in the future discussing our process and the specific types of businesses that we like to own for ourselves and our clients. However, for this market review we thought we would dedicate some time to macro environment. We were recently asked to make a presentation to a group of investors here in Santa Barbara about this topic, and because it is currently garnering so much media attention (justifiably so), thought we would share some of our observations from the presentation with you.

THE MACRO PICTURE

The Macro Economic back drop of course plays a part in our process. It is particularly important when it comes to trying to insure our portfolio against risk associated with prevailing current monetary and/or fiscal policy, or as we like to jokingly think of it “Dylan Risk”.

Clowns to the Left of Me, and Jokers to My Right,

Here I am stuck in the middle with you

– Bob Dylan

In short – we cannot overstate how important it is to discount the near daily market opinions being spoon fed to the media by politicians, and market experts alike — If for no other reason than these folks are so often wrong. Take the following quotes from our recent housing bubble:

“I think it is clear that Fannie Mae and Freddie Mac are sufficiently secure so they are in no great danger… I don’t think we face a crisis; I don’t think that we have an impending disaster. …Fannie Mae and Freddie Mac do very good work, and they are not endangering the fiscal health of this country.” Congressman Barney Frank – October 2004

Co-Author Dodd-Frank Bill on Financial Regulation

“Fannie Mae and Freddie Mac should be abolished … There are people in this society who for economic and, frankly, social reasons can’t and shouldn’t be homeowners … I think we should, particularly, stop this assumption that you put everybody into homeownership.” Congressman Barney Frank – August 2010

“American consumers might benefit if lenders provided greater mortgage product alternatives to the traditional fixed-rate mortgage.” Federal Reserve President Alan Greenspan – February 2004

“It looks as though the worst is behind us in terms of the effect of the housing slump on economic growth” Former Federal Reserve President Alan Greenspan – November 2006

“The sub-prime mortgage fallout is largely contained”

Hank Paulson, US Treasury Secretary

Ben Bernanke, Federal Reserve Chairman

George W. Bush, President – March 2007

We think the above statements beg the following question — What is the likelihood that the same people who missed the crisis to begin with will be able to identify and implement the correct response?

Let’s look at our Government’s approach to the recent economic crisis. In this case we have seen the Fed and Congress intervene to lower rates and increase leverage (or at least transfer leverage from banks and individuals to the federal government’s balance sheet) in order to address a crisis in large part created by – you guessed it – leverage and very low interest rates. Fortunately for us at Alamar, we don’t have to make these types of difficult decisions. What we do have to do though, is determine how this policy will affect the positioning of our portfolio and the potential impact and consequences it will have on the overall economy. Our predominant current concern is inflation. Simply put, you can’t run deficits at 10% of GDP for three years in a row and expand the Feds balance sheet from $900 Billion to almost $3 trillion without an eventual impact. Furthermore, given their batting average and the difficulty of the task involved, we believe it is unlikely that the Fed will appropriately time and address the need to alter rates to offset this inflationary pressure (Please see Exhibits – Next Page).

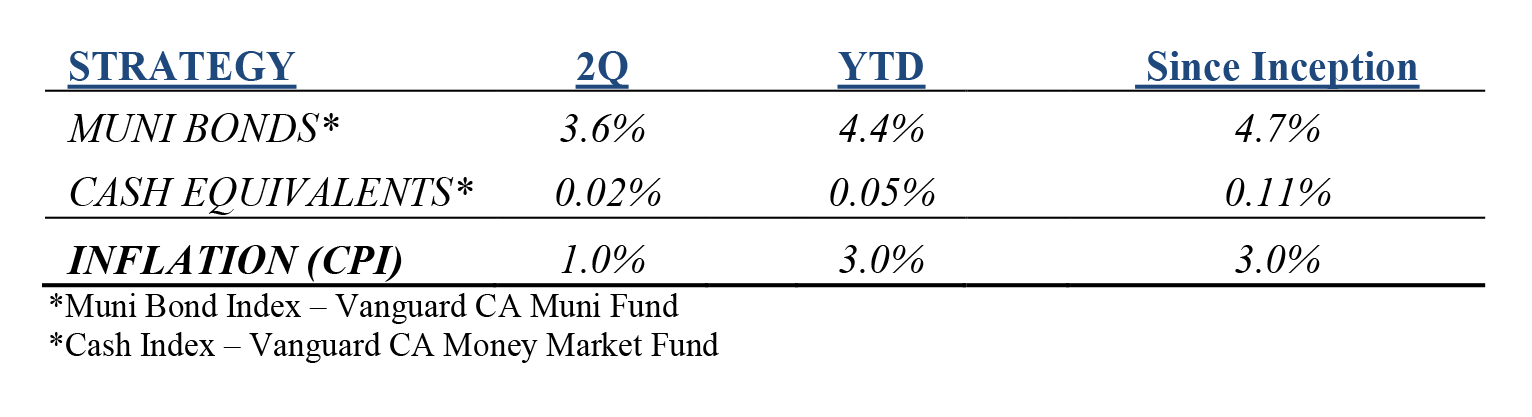

Thus far, it is debatable this policy has had the intended result of creating jobs. It may have saved some, but this is conveniently difficult to quantify, as is the argument the crisis would have been much worse if we had done less, or nothing. The reality is that we will never know. What is not debatable, however, is that with real interest rates at -3%, and bond rates at historic lows, it is unlikely that many risk-averse investors, with large allocations to cash and bonds, realize the actual risks they are taking. The chart below provides a helpful example of the extent to which some of these strategies have been able to combat inflation and preserve purchasing power since our All Cap Strategy’s inception, January 1, 2010.

In the meantime, Alamar’s portfolio of companies continue to see their revenues and earnings grow. They are highly profitable, rich with cash, have low levels of debt, and reasonable valuations. Granted, the ride in equities is, has, and will continue to be bumpy — with sovereign debt issues abroad (we will see some defaults eventually) and the need for an increase in the US debt ceiling (a very likely outcome in our opinion), we still believe the journey in the stock market is worth it, and will be more favorable to many alternatives over time.

Best regards,

John Murphy, CFA

john@alamarcapital.com

George Tharakan, CFA

george@alamarcapital.com